The Prudence Of Penny-wise Preparedness

Let’s say your car breaks down tomorrow; it’ll cost you $1,000 to get it back on the road. You have no other vehicle, and you need this one to get to work and back. Could you swing the expense? What if it were $500? For far too many people, even $100 would throw their entire budget out of whack.

One of the best preps you can accomplish is to get your financial house in order. As anyone who’s been there will tell you, the more broke you are, the more often the smallest emergencies seem nearly insurmountable.

Nobody likes having to pay an unexpected $100 for a car repair, but when doing so means you might have to skip a meal or two for the next few days, that’s a big deal.

While financial planning might not be as “sexy” as knives or fire kits, it should definitely be part of your overall approach to preparedness. Remember: A personal financial disaster can be almost as devastating as a natural disaster.

Let’s take a look at several key components.

Reducing Debt

One of the first steps toward solid financial footing is to lower the amount of money that needs to go out each month. This is arguably the most difficult part of the equation, no question about it—but it can be done.

One of the biggest mistakes people make is to constantly hope for some huge windfall that will fall out of the sky and allow them to pay off all their bills in one fell swoop. The reality is that it takes hard work and grinding away at debt a little every day.

“… SHOULD CURRENCY SUDDENLY BECOME WORTHLESS, IT MIGHT NOT BE THE WORST IDEA TO HAVE TANGIBLE ITEMS AVAILABLE THAT YOU CAN TRADE FOR THINGS YOU NEED.”

Make a list of every revolving credit account you have that carries a balance. This would consist of things such as credit cards and store cards. Go down the list and call each of them.

Ask if there’s anything they’d be able to do to help you out with getting your balance paid off quicker, such as temporarily reducing your interest rate. Sometimes, they’ll work with you; sometimes they won’t, but it never hurts to ask. Even if they only reduce your interest rate for a couple of months, that’s better than nothing.

Next, go down the list of accounts and find the one with the smallest balance. Pay as much as you can possibly afford toward that bill while still paying at least the minimum due on everything else.

It won’t happen overnight, but once that bill is finally retired, take the money you were paying on it and put it toward the next-lowest balance on your list, adding it to whatever you were paying as the minimum.

Over time, if you stick with it and don’t incur much in the way of new charges, you’ll get the accounts paid off. You’ll also find that the payoffs come quicker as you go along, because you’ll be putting more and more toward an account as you eliminate bills from the budget.

In addition, always be on the lookout for ways to speed up the process. For example, from time to time, credit card banks will send out offers for balance transfers that include a no-interest grace period. Read them carefully, and if you’re able to swing it, these can be great for allowing you to pay off accounts faster.

However, the devil’s in the details, as they say: With some offers, if you don’t pay the balance in full by the end of the grace period, the full accumulated interest might be tacked on.

The best approach for this is to divide the expected balance by the number of months in the grace period. If you can’t commit to making those payments each month, take a pass.

Increasing Income

If you’re able to bring in a few extra dollars each month, that’ll help with either paying down bills or building up an emergency fund. As with debt reduction, don’t concentrate on finding that huge payoff, because that probably won’t happen.

Instead, work on coming up with practical ideas that’ll bring in a steady income. As long as you’re earning more than you’re spending to do it, consider it a win.

Do you have any hobbies you might be able to monetize without much effort? Let’s say you enjoy gardening. In the spring, maybe plant some extra seeds and then sell the seedlings to friends and neighbors. If it takes off, you might eventually get a stand at a local farmer’s market.

There are many opportunities online for creative types such as writers and artists. Websites such as Fiverr.com work well for connecting content providers with clients. The nice thing about this kind of work is that it can generally be done on your schedule, even if that means just a few minutes here and there over the course of a week.

Other suggestions include:

- Selling crafts, either online or at local flea markets and similar venues

- Repairing small engines, such as lawnmowers and snowblowers

- Doing odd jobs around the neighborhood, such as cleaning gutters, mowing lawns or cleaning pet yard waste

During the recent lockdowns, one enterprising person in my area started a delivery service. He’d pick up just about anything you requested from local stores and would bring it to your home for a small fee.

While many restaurants would deliver food to customers, gas stations and convenience stores certainly weren’t delivering cigarettes or beer. For some folks, those items fall into the “necessity” category. He’s just one example of someone who saw a need in the community and found a way to make an honest buck filling it.

Put Your Credit Card to Work

This is something that requires incredible discipline, but if you can manage it, the payoff is pretty good. I have a credit card that offers cash-back rewards for use. Over the last few years, I’ve used this one card to pay almost all of our family’s routine bills and purchases—from car and mortgage to groceries and gas.

Each month, the balance is paid in full, so I don’t incur interest charges. We’re not spending any more money than we would be otherwise; we’re just running everything through this one account. This really racks up the rewards, and we’ve earned several hundred dollars since I began doing it.

Again, this isn’t an approach for those who lack willpower, because it’s awfully easy to fall into the credit card “trap”—buying everything today with plans of paying for it tomorrow. But, if you’re able to keep it under control, this can be a good way to bring in a few extra bucks while not spending a nickel more than you do now.

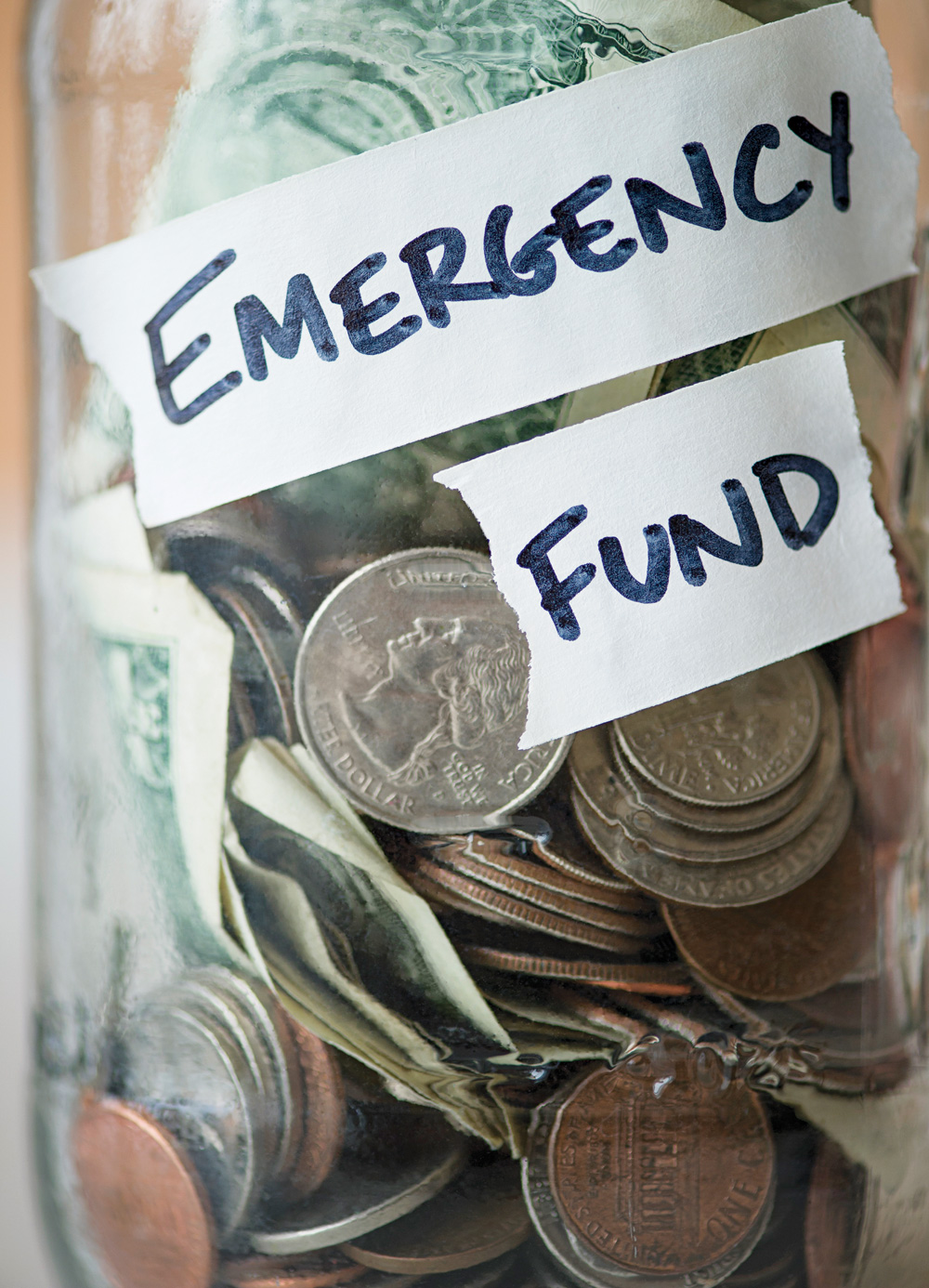

Establish an Emergency Fund

As you’re able to free up some cash in the budget, work on putting some of it aside for a “rainy day.” This should be separate from any funds you’re saving toward a goal such as a vacation or new vehicle.

The idea behind having an emergency fund is that it isn’t touched, except in an actual emergency. Spending it on a new rifle or ATV means it won’t be there when the water heater quits.

Outside of unexpected repairs to home or vehicle, probably one of the biggest reasons to have an emergency fund is in case of sudden unemployment. Gone are the days when someone could expect to be hired by a company, work for it for 30 years and then retire with a full pension and other benefits.

Unfortunately, today, unexpected downsizing and business closures are common. It can take weeks or even months to find new employment, at least in terms of a job that pays a sustaining level of income.

How much should you set aside for emergencies? Shoot for at least enough to cover all your bills and expenses for one full month as a minimum. However, don’t stop there: Keep adding to it with every paycheck. The ideal would be to have enough to live on for several months. Even if you’re only able to afford a few dollars each week, it’ll add up over time.

This money could be kept at home if you have a secure place to put it, such as a fireproof safe. Otherwise, a bank is probably your best bet. Remember: We’re not prepping for a complete and total societal collapse here; we’re just trying to sock some money away to pay our rent or mortgage if times get tough for a bit.

Barter Goods

There are some who’ll tell you—with sincere conviction—that money will be worthless after a major collapse. They might very well be right. But, until that happens, cash is what makes the world go ’round. Money is worth something right up until the point that it isn’t.

That said, as preppers, we like to cover as many bases as we can. So, should currency suddenly become worthless, it might not be the worst idea to have tangible items available that you can trade for things you need.

Here are three guidelines to consider when choosing items to stock up on for later use in bartering:

- The item should have inherent use for yourself or your family. In other words: The day for trading might never come, so make sure you’ll have some use for the item anyway.

- The item should be fairly inexpensive now but be likely to have good trade value later. It makes very little sense to spend a ton of money stockpiling barter goods when you could be spending that money stocking up on what you’ll need so you won’t have to barter.

- The item should be shelf-stable or otherwise easy to store for a long time without going bad. The last thing you want is to finally need to trade with someone, only to find that your barter goods are now worthless.

If you stick to the name brands, disposable lighters can last awhile and make for great trade material.

Here are some suggestions for useful barter goods:

- Candles

- Canned food

- Disposable lighters

- Hand tools

- Salt

- Soap

- Toilet paper

Offering ammunition in trade is discouraged—if only because the recipient might decide to “return” it to you at high velocity later. Obviously, if the person is a trusted member of your circle, that shouldn’t be an issue.

Precious metals are often mentioned as a form of backup currency. There are a couple of potential pitfalls with this approach. Bear in mind that if all you have are gold coins, then anything you might need to buy now costs a minimum of one coin. In other words, it can be nearly impossible to make change for this sort of transaction. On top of that, you might very well run into people who are reluctant to accept precious metals simply because they lack the ability to determine if they are genuine or not.

Another aspect of this is to consider what skills you have that could be used for trade. What work could you perform to earn what you need from someone? For example, if you’re handy with tools, you might be able to help neighbors with home repairs and such in exchange for a bit of their garden produce. Or, if you’re the gardener, maybe your neighbor will help you can and preserve the food for a small cut. Maybe you’re excellent with hunting and trapping and you have a close friend who is a far better cook than you.

Keep in mind that bartering only works if you have something someone else wants or needs, they have something you want or need, and you both know the other exists. That last part is a key element. If your plan is to essentially disappear in the wake of a major event, barter and trade might not be in your future.

One last bit of advice when it comes to finances and disaster planning. It makes very little sense to put yourself into a poor financial position now by prepping for something that might happen someday. In other words, don’t get so wrapped up in the preparedness part of life that you end up in danger of foreclosure or bankruptcy. Strive for a workable balance between the two.

Money in the BOB

In a typical emergency evacuation, the vast majority of problems you’ll run across can be resolved through the use of a cell phone, credit card, or cash. I know this flies in the face of much of what you’ll read in survival and prepper literature, but it is the simple truth.

Separate from your emergency fund, consider setting aside funds for your bug-out bag or other evacuation kit. A good goal is to have enough cash on hand to allow you to fill up your vehicle, feed your family for a couple of days, and pay for at least two nights in a decent motel.

Doing so will give you options should the time come that you need to beat feet with a quickness. It is a judgement call as to where to keep the funds. Depending on your individual situation, it might make sense to keep the money in a safe or other accessible location rather than in the BOB itself.

Estate Planning

Part of getting your finances in order should include planning for your ultimate demise. Despite our best efforts, none of us are going to get out of here alive. When my father passed in July, 2019, he left behind a rather sizeable mess. His will was about as bare bones as it gets, extremely vague and decidedly unhelpful.

He had no life insurance, no savings, nothing at all, so everything landed on our shoulders. My wife and I incurred tens of thousands of dollars in expenses from the funeral, home repairs, storage fees, and more. It took us months to get his affairs squared away, as well as empty his home and get it ready for sale.

If you have loved ones, don’t do this to them. Make solid plans for what you want to happen upon your death and communicate those wishes to everyone. On top of that, do everything you can to ensure there are funds available to pay for your last wishes and to settle your estate.

Editor’s note: A version of this article first appeared in the October, 2020 print issue of American Survival Guide.